As countries across the globe went into COVID19-induced lockdown with much of our ordinary lives and routines on hold or cancelled until further notice, market participants scoured for liquidity with stock exchanges closures and price behaviours unimaginable to date.

S&P 500 triggered wide circuit breakers four times in the space of nine days at the end of March and local exchanges in frontier markets like Bangladesh, Sri Lanka, Jordan and Palestine being closed throughout April. These jittery tensions reached the index providers. The index rebalances postponement that was announced by S&P Dow Jones Indices, FTSE Russell and ICE Data Service may have appeared trivial. After all, there were and still are some bigger survival questions to answer.

The index rebalance delays would be inconsequential, if not for changing market dynamics over the last decade, meaning financial indices are not mere barometers of the state of financial markets as they once were. In fact, they are now used by the wide investment community and researchers for a variety of purposes.

Academics use benchmarks as a market proxy to study price discovery mechanisms and market behaviour patterns. Meanwhile, asset owners, fund managers and broker-dealers use indices to track and measure performance, with a large proportion of investment funds directly replicating the indices.

Index-tracking funds and ETFs which track the return on the index have now swelled to 30 per cent of total fund assets in 2017 in the EU, while passive funds are around 43 per cent of total equity fund assets in the US. As such, indices are determining the investment universe and substantially influencing price discovery, price signalling and the flow of financial capital.

What is a ‘good’ financial index?

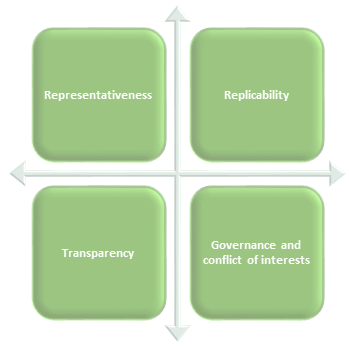

As indices became a critically important canvas of the financial system, the discretionary decisions in March delaying or cancelling reconstitution of some benchmark providers raises complex questions on governance and accountability. The main qualities of a ‘good’ benchmark that will help the portfolio manager to achieve the targeted market exposure by replicating the index generally satisfy the following criteria:

- Representativeness of the choice set available to gain specific asset access

- Replicability of the index through its investable universe criteria (e.g. market access, liquidity criteria) and timely dissemination of all relevant index data

- Transparency of the rule-based methodology and index maintenance

- Governance and conflict of interests arising from calculation and maintenance of the index.

These are the guiding principles that must be met, for instance, for the index to be eligible as an adequate benchmark for investment by UCITs (Undertakings for the Collective Investment in Transferable Securities), a regulatory framework for ETFs registered and distributed in Europe.

Recent index rebalance delays, however, raise a question over the discretion that index vendors can have in taking an active decision affecting the composition of the index, the target of which is to reflect the market as guided by a precise and transparent index methodology.

While the decision to postpone rebalances may have had the best intentions and merits, of protecting index funds and ETFs holders from disrupted market conditions, trading halts on certain exchanges and larger bid-ask spreads, it most certainly had direct and indirect consequences, too.

What were the observed costs of index delays?

Into the category of direct costs fell hedge funds arbitraging around index rebalances, which reportedly suffered losses due to positioning for the expected index reconstitution that was supposed to happen at the end of March. Hedge funds and some enhanced passive strategies build up positions weeks before the rebalance by placing programme-led index trades predicting index reconstitution. Since the index follows a clearly defined methodology, under normal circumstances, such reconstitution is predictable. Unless, of course, the index decides not to rebalance; as some did in March this year.

Another concern for index postponement is that it changes the investment outcome of the targeted market exposure. Take an equally-weighted index with a clear mandate to allocate each constituent a fixed weight, such as the S&P 500 Equal Weight Index. A delay in rebalance means that the index does not fulfil its index criteria to maintain economic reality as represented by the investment opportunity set based on a market, segment, theme, or investment.

For instance, Invesco is paying $105m to shareholders in its $5.6bn Equally-Weighted S&P 500 fund (VADDX), and its variable insurance version for misunderstanding an adjustment S&P made to delay the rebalance of the index the fund tracks during this volatile market period in March. What’s more, fund managers, struggling to digest the market turbulence and almost unheard-of decision not to rebalance the main suite of indices, were caught out.

How much discretion do benchmark providers have?

Although indices are guided by criteria as set out by the methodology and index policy rule books, it may come as a surprise to some how much discretion index vendors have in the area of corporate actions, governance and determining the opportunity sets within specific asset classes, industry or country.

For example, voting rights and dual share class issues widely debated over the last couple of years by index users and index providers meant that some benchmarks took a diverging view on the application to the investment universe. Following 18-month consultation with market participants, MSCI decided to include shares with unequal voting structures for its main indices. S&P, on the other hand, has ruled out companies with multiple share classes defending its position of ‘one share, one vote’ and the importance of voting rights for a well-functioning market with accountability mechanism.

Another example of where the discretion by index may be used is country classification and a classic example of Korea and China A-shares. The choice to classify as a developed versus emerging, or decision to include in emerging market universe has substantial consequences for the flow of funds in these markets and reflects varying investment opportunity sets. Indices have had their different opinions on this too.

How COVID-19 raises financial indices governance questions

As a result of market upheaval and such index rebalance postponement in March 2020, a number of benchmark providers have had to update their index policies with regards to the use of discretion in disrupted markets. MSCI, for example, updated its index policy documents on the definition of ‘material change’ to the index, adding the discretion to exercise the right of ultimate decision-maker. Elsewhere, Solactive issued a ‘disruption policy’ setting out rules and procedures for index calculation during conditions of market stress, voluntary and regulatory trading halts.

Indices became a critically important canvas of the financial system, while discretionary decisions in delaying or cancelling reconstitution raise some complex questions on governance and accountability. We are left with the question: can benchmark providers balance their discretionary powers in the interest of all stakeholders in this landscape?

Disclaimer

Ryedale publications do not offer investment or trade advice or make recommendations to use any particular investment strategy. Should you undertake any such activity on the basis of information contained in Ryedale publications, you do so entirely at your own risk, and Ryedale shall not be held responsible for any loss, damage, costs or expenses incurred by you as a result.

The information we publish has been derived from or is based on sources that we consider to be accurate and primary. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. You should always carry out your own independent verification of information and seek a professional advisor before making any investment decisions.