Recent years have seen a proliferation of ETFs launched to capture all sorts of investment ideas. The break-even point for an ETF depends on many factors, not least the scalability of the sponsoring firm's platform. It's fair to say that many sponsors see the $1bn assets under management (AUM) threshold as a real coming-of-age for a fund. It is a point where you can be sure the fund is contributing to the house, rather than needing the support of the house. So, what proportion of ETF launches make it to this threshold?

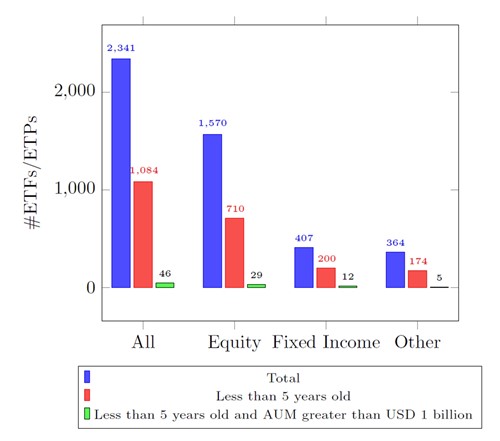

We examined launches of ETFs in the US in the five years to 1 January 2020. Out of those that survived up to the end of 2019, only 4.24 per cent managed to reach $1bn in AUM. In today's world of super-low fees, many firms consider $1bn as the break-even point required to achieve comfortable profitability. The odds are only slightly higher for fixed-income funds, standing at one in 17. And the actual numbers are even lower once the effect of the survivorship bias is accounted for.

Source: ETFdb.com

A big reason for such a low success rate is the proliferation of novel investment strategies, making the ETF market extremely crowded. Some 46 per cent of the US-listed funds available today were launched after 2015. ETFGI reports that the total AUM of ETF/ETPs surpassed $6tn globally – an extraordinary growth of over 100 per cent in five years.

At the same time, the average profit margins are falling: J.P.Morgan finds that ETF fees fell by more than 40 per cent in the US since 2012. Such a decline is projected to continue. For example, in December 2019, this competition forced the creation of the first negative fee ETF (Salt Low truBeta US Market Fund).

Reasons for Growth

Poor performance of active managers

Investors' general disappointment in the returns of underperforming hedge funds and mutual funds, together with a much higher fee structure for such products, makes it unsurprising that active funds have experienced an outflow of more than $500bn over the last 15 years. Active strategies are slowly being integrated into a much cheaper ETF structure.

Conducive regulatory environment

Legislation such as RDR in the UK and MiFID II in Europe facilitated the flow of retail money to ETF products. Both banned the long-standing practice of wealth managers directing retail and professional clients' money towards mutual funds with the highest commission arrangements. In addition, recent changes to Exemptive Relief regulation adopted by the SEC in the US make it much easier and faster to launch an ETF fund.

Tax Efficiency of ETFs

ETFs are generally more tax-efficient than mutual funds as they are flexible in recognizing taxable gains. For instance, outflows from mutual funds force portfolio managers to sell the underlying stocks in cash. This can lead to significant taxable gains for mutual fund holders. In contrast, redemptions on ETFs can be done in-kind with authorized participants (APs). To minimize taxable gains, portfolio managers can choose to transfer those securities with the lowest tax base.

Improvements in Technology

Employing modern technology when dealing with a growing variety of data providers and complex benchmarks has proved to be a fundamental factor for success. Not only has it allowed many ETF issuers to develop differentiated product offerings, with funds of varying complexity and size, but it has also made it possible to scale.

Striving to Survive

Given the hostile environment in which ETF issuers are not able to compete on fees, they often choose one of the two approaches to differentiate themselves.

Alternative exposure and innovative indexation

It is possible to focus on new asset classes or on the introduction of new themes that provide a unique or targeted risk exposure. Ideally, these should have a low correlation to traditional investment strategies. Recent examples are Cannabis, Artificial Intelligence or Work-From-Home ETFs. However, it can be difficult to generate sufficient asset flows since such investment ideas may not have broad appeal. There may also be technological barriers. The data required to implement such investment ideas may be complex or costly to acquire, and it may be challenging to integrate that into the portfolio management process.

Compete by minimizing tracking error

A low tracking error is the most desired characteristic of an index fund by industry professionals. However, it requires the constant diligence of the investment team backed by good technology which can highlight sources of tracking risks before they happen. Question marks over capabilities to consistently produce low tracking error has led some large asset managers, who otherwise would be well placed to be successful ETF sponsors, to stay out of the ETF marketplace.

ETF Lifeline

The Ryedale Platform is a leading investment management software and service solution which can help fund managers with all aspects of managing ETF portfolios. It contains a wealth of tools to make the management of ETFs easy. From projecting an index-change to producing an optimal trade list, from creating standard PCFs to custom in-kind baskets, from tax optimization to managing currency exposures: all the tools to streamline every step of the investment process are integrated into a single, easy user experience.

Efficient integration for multiple data sources

While ETF portfolio managers may wish that benchmark data consumption becomes a smooth operational routine, it may be hard to achieve in practice. Sourcing, mapping and validating data remains a key step of robust index fund management processes. The Ryedale Platform is an expert in consolidating index data feeds from a broad range of established and emerging benchmark providers as well as supporting internally constructed custom benchmarks. Data sets, regardless of origin, are consumed, validated and stored consistently and seamlessly in the cloud-based service, thereby eliminating the need for a separate benchmark management system.

Reconciling data discrepancies

The Ryedale Platform records every trade and every position of every fund, independently of accounting or custody data. It maintains a full investment book of record (IBOR). This allows investment teams to reconcile the custodian positions, as well as any other datapoints, against internal positions and to detect any variations. Stale or erroneous data can result in suboptimal trading decisions and contribute to tracking error.

Compliance

Continuous monitoring and reporting on all portfolios are built into the Ryedale Platform. This ensures that compliance rules for those portfolios are not breached. Customizable compliance rules help to make sure that portfolio managers act in accordance with investment mandates and regulatory restrictions, including short-selling and concentration limits.

Significant market transformations happening over the recent decade have resulted in a booming marketplace for ETFs. Yet, despite both AUM and number of ETF products increasing rapidly, the statistical evidence is that successful ETF products are difficult to create. There is a clear barrier for ETF AUM that is hard to overcome. Given the proliferation of competing product offerings, ETF managers need to develop deep competence in running many index funds at low cost and with consistently low tracking error. Having a robust technology backing the portfolio managers is becoming a necessity to survive.

Disclaimer

Ryedale publications do not offer investment or trade advice or make recommendations to use any particular investment strategy. Should you undertake any such activity on the basis of information contained in Ryedale publications, you do so entirely at your own risk, and Ryedale shall not be held responsible for any loss, damage, costs or expenses incurred by you as a result.

The information we publish has been derived from or is based on sources that we consider to be accurate and primary. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. You should always carry out your own independent verification of information and seek a professional advisor before making any investment decisions.