The continued growth in index-based strategies over the last decade has resulted in a multifaceted landscape of financial benchmarks with a wide variety of indexes of various themes, styles and construction approaches.

Indexes are governed by rules-based methodologies and, typically, rebalance regularly. This is done in order to maintain the representativeness of the specified market exposure and to ensure the methodology continues to reflect its stated objective. For the indices to be replicable, index providers set out schedules for the reconstitutions and announce changes in advance of the rebalance day. At that point, the benchmark changes its constituents and respective weights.

Is tracking an index a passive exercise?

Rebalancing schedules vary between index strategies and benchmark providers. Differences in how indexes are calculated and rebalanced are usually determined by their construction methodology, choice of rebalancing frequency and the timing of the review.

Although a typical index rebalance schedule is quarterly or bi-annually for a market capitalisation strategy, it can be more frequent - monthly or even daily - for factor and style strategies, such as low volatility. Frequency can also be triggered by conditions specified in the index vendor methodology and is often specific to the type of index construction approach.

It may come as a surprise to some that indices never ‘sleep’. They may be frequently rebalanced outside of ordinary schedules due to index changes associated with corporate action events, such as mergers and acquisitions, spin-offs, partial tender offers and capital repayments.

All this is crucial for passive fund managers who run their strategy with the objective of replicating the index and achieving targeted market exposure. Like the indices themselves, fund managers have to be vigilant. So, while a passive management approach is associated with following the index without taking active bets, replicating an index itself is anything but passive. It is an elegant balancing act of index changes, corporate actions, liquidity, local market access, client flows, trade costs and tracking error.

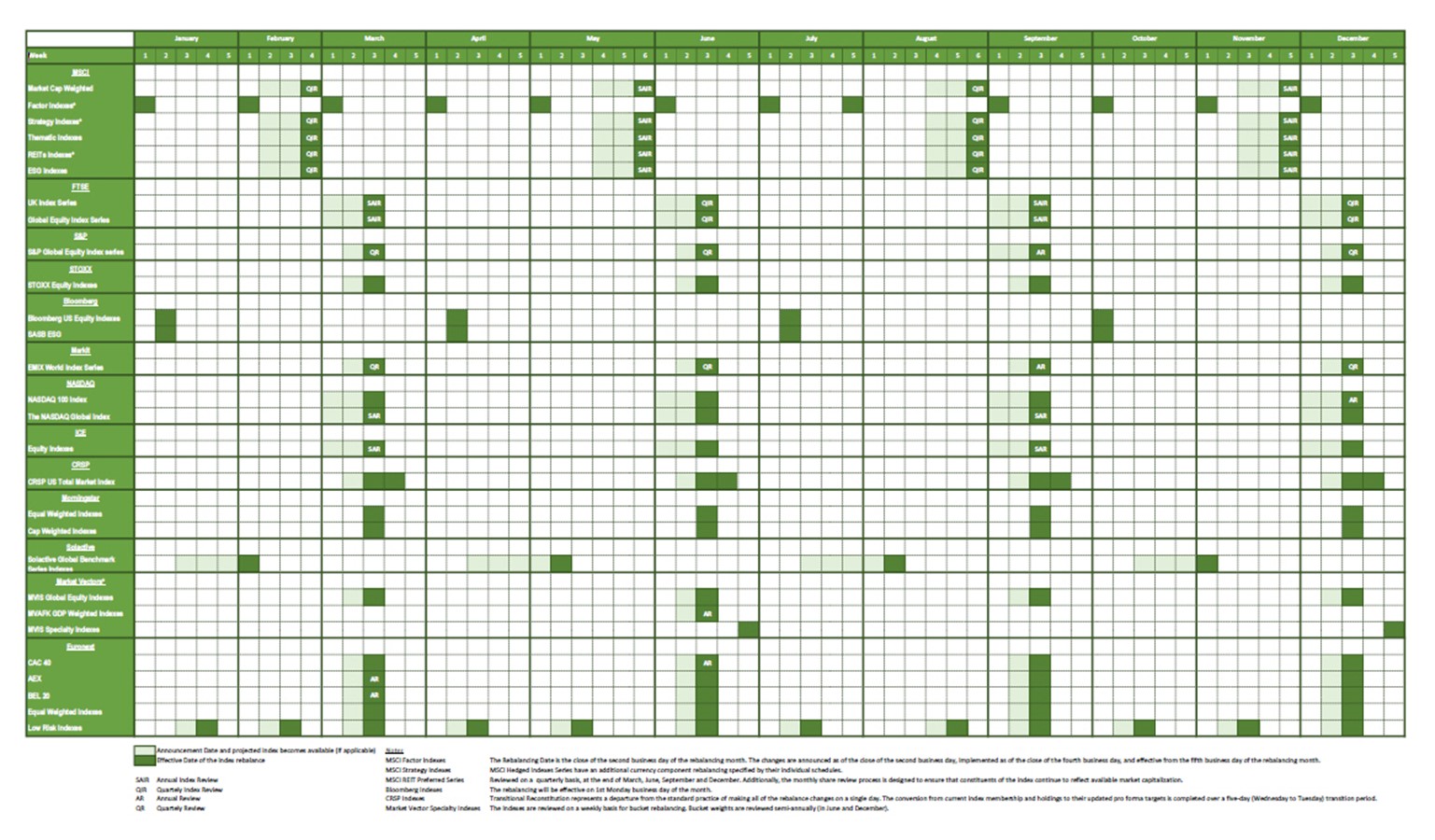

What does the rebalance schedule look like?

In light of the upcoming MSCI August Quarterly Rebalance, we have constructed a matrix to track the biggest index providers’ rebalancing schedules on most notable indexes. The Index Rebalancing Matrix is a simplified calendar designed to draw attention to important rebalancing points and announcements that precede their effective dates. The list is not exhaustive but acts as an illustration of the approaches taken by a variety of index vendors.

The calendar highlights that many providers take a quarterly approach to rebalancing and commonly rebalance in March, June, September and December. However, MSCI, with $13.1tn of assets under management benchmarked to its indices, rebalances its market capitalisation indexes in February, May, August and November. Bloomberg also undertakes quarterly rebalancing but starts in January, in contrast to most of the other main index providers. Meanwhile, CRSP’s methodology represents a departure from the standard practice of making all of the rebalance changes on a single day. To avoid market impact, the conversion from current index membership and holdings to its updated pro forma targets is completed over a five-day transition period.

Regardless of the rebalance effective date, most providers offer announcement dates in advance of the effective rebalance date: generally anything between two and 20 business days leading up to it. However, predefined by methodology rebalance schedules are not static either. Recent events during extreme market volatility in March 2020, when a number of benchmark providers decided to postpone their scheduled rebalance, is a testimony to that.

Index Rebalance Matrix. Source: Ryedale

What is the market impact of the index reviews?

Despite emerging evidence of the index effect weakening*, benchmark providers are constantly reviewing their approaches in rebalance implementation to uncover more efficient ways to manage index reviews. They assess potential to limit market impact (bid/offer size), transaction costs and ease replication of indices. MSCI, for example, launched a consultation in August 2020 on assessing the market impact of its index reviews and offering a ‘staggered’ implementation approach. Such implementation would imply a transition from base to ‘pro forma’ index over three days, rather than in one go. A ‘light’ rebalancing scenario under conditions of market stress is also being considered**. All these varied approaches and differences in the index providers rebalance schedules makes running passive strategies an intricate and complex balancing act.

How Ryedale can help

Having an effective portfolio management system which loads index and projection files automatically with upcoming rebalance data and its impact certainly helps. Through the choppy waters of March 2020 rebalances, we have seen what the cost can be of omitting such important information. The data management master is built into Ryedale Platform with indexes in mind. This means that when the fund manager checks the upcoming index rebalances; the size of the mis-weights between the fund and the benchmark; and the impact of changes and suggested actions; the answer is right there, just a click away.

*The Index Effect is the phenomenon where stocks that are added to an index experience positive excess returns in the days before being officially added, while stocks that are removed from an index experience negative excess returns.

**(QIR) rebalancing to replace a SAIR in times of extreme market volatility to reduce the rebalancing impact.

Disclaimer

Ryedale publications do not offer investment or trade advice or make recommendations to use any particular investment strategy. Should you undertake any such activity on the basis of information contained in Ryedale publications, you do so entirely at your own risk, and Ryedale shall not be held responsible for any loss, damage, costs or expenses incurred by you as a result.

The information we publish has been derived from or is based on sources that we consider to be accurate and primary. Although reasonable care has been taken, we cannot guarantee the accuracy or completeness of any information we publish. You should always carry out your own independent verification of information and seek a professional advisor before making any investment decisions.